How To Estimate A Variable In Stata

Before you can begin estimating models you need to import the data into Stata. Variables can be either observed exist as variables in your dataset or unobserved.

Receiver Operating Characteristics Roc Stata

Notation to override the default and tell Stata that age is a continuous variable.

How to estimate a variable in stata. Section 4 provides ex-amples of how to get variance components estimates in Stata for several experimental designs. The egen command treats missing values as 0. To create a new variable for example total from the transformation of existing variables for example the sum of v1 v2 v3 and v4 use.

Well I have a set of 6 independent variables X1 X2 X3 X4 X5 X6 where X5 and X6 are dummy variables. We use the pwcorr pairwise correlation with the sig option to get a p-value with the estimate. One variable appears on the left-hand side of the equation.

To know how well the predictors taken together as a group reliably predicts the dependent variable Stata conducts an hypothesis test using the F-statistics. ECO372 Stata How-to. In order to test the -re- estimator against the-fe- estimator I wrote the following syntax in Stata.

2mean Estimate means Syntax mean varlist if in weight options options Description Model stdizevarname variable identifying strata for standardization stdweightvarname weight variable for standardization nostdrescale do not rescale the standard weight variable ifinover overvarlist o group over subpopulations defined by varlist o SECluster. Egen total rowtotal v1 v2 v3 v4 Note. I am trying to estimate the mean of a variable for 2 different groups.

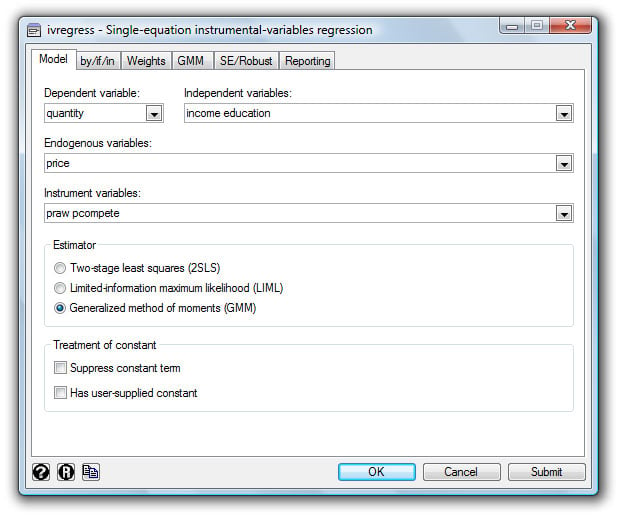

In a simple regression only that is when there is just a single independent variable the R2 is exactly equal to the Pearson correlation between the two variables. Instrumental Variables Estimation in Stata The IV-GMM estimator We consider the model with X N k and define a matrix Z N where k. Alternatively use egen with the built-in rowtotal option.

Which are your outcome and predictor variables. This is the Generalized Method of Moments IV IV-GMM estimator. When we perform linear regression on a dataset we end up with a regression equation which can be used to predict the values of a response variable given the.

This method should distinguish basically between time-varying and time-invariant regressors as follows. The varbasic command allows us to fit s simple reduced-rorm VAR without constraints and graph the impulse-response functions IRFsThe more general var command allows for constraints to be placed on the coefficients. Expectations of future variables appear within the E operator.

Basic syntax 1 2. Using Stata 9 and Higher for OLS Regression Page 4. The instruments give rise to a set of moments.

ARIMA models are popular to estimate demand of products or services sales production quotas financial stocks and other economic variables such as CPI. By doing it this way. Hence we use the c.

Rather the AME estimates the partial effect of the variable x on the outcome variable y for using the observed values for the covariates and then the average of that partial effect is estimated. Further each variable in the model appears on the left-hand side of one and only one equation. Example 2 Imagine we would like to estimate the following model.

Your purpose in including them has been accomplished and would not be accomplished any better with a non-multicolinear set of variables carrying the same information. The null hypothesis is that the mean explainable variance is same as the mean unexplainable variance. Section 2 describes the ANOVA method for estimating variance components and demonstrates how ANOVA-type estimates can be obtained using Stata.

In other words that residuals residuals are systematically different. In that case we can use the Hausman-Taylor estimator xthtaylor a transformed Random Effect RE model with instrument variables IV. Instrumental Variables using 2SLS 2019-09-16 Contents 1.

Sum variable Ill get the mean. Gen total v1 v2 v3 v4. However there are differences among two groups in terms of age gender education.

We do not want or need to compute the variable separately. Pwcorr vote_share mshare sig. If the standard error of a focal predictor that is of a variable whose effect your goal is to estimate is inflated then you have a multicolinearity problem.

To again test whether the effects of educ andor jobexp differ from zero ie. Expression is a formula made up of constants existing variables operators and functions. Not greater than.

G i β Z0ui Z0yi xiβ i 1N where each gi is an -vector. Before running a regression it is recommended to have a clear idea of what you are trying to estimate ie. Be aware that for most macroeconomic variables ARIMA models can provide some insights ie inflation money supply GDP etc however there are more sophisticated models you can estimate such as VAR models.

0 1 and 7 control variables X7 X8 X9 X10 X11 X12 iSECTOR_ where X7 and iSECTOR_ are dummy variables. In a multivariate setting we type. Additional controls 2 3.

To see this run. So cagecage tells Stata to include age2 in the model. The method of moments approach.

Regress y x1 x2 x3. Xtreg Y X1 X2 X3 X4 X5 X6 X7. Nestreg command is particularly handy if you are estimating a serieshierarchy of models and want to see the regression results for each one.

Relational Arithmetic Logical numeric and string addition. Estimation using Stata For simple VAR estimation with Stata we will use the varbasic command. Yi xi ei 1 However we suspect an endogeneity problem.

Some examples of expressions using variables from the auto dataset would be 2 price weight2 or sqrtgear ratio. Before we can use quadratic regression we need to make sure that the relationship between the explanatory variable hours and response variable happiness is actually quadratic. Section 3 dis-cusses xtmixed as a tool for variance-components estimation.

If in Stata I use. Gen newvar 0. Since Stata automatically deletes the time-invariant regressors they cant be estimated by ordinal methods like FE.

The operators defined in Stata are given in the table below. How to Obtain Predicted Values and Residuals in Stata Linear regression is a method we can use to understand the relationship between one or more explanatory variables and a response variable. You are on the right track to start mastering Stata and learning how to estimate diverse economic models which will help you conduct your research or do assignments.

Regress dependent variable independent variables regress y x. In this first tutorial I will teach you how to Generate time series variables in stata. To test β 1 β 2 0 the nestreg command would be.

In Stata use the command regress type. Use the following steps to perform a quadratic regression in Stata.

Basic Statistics Stata

How To Describe And Summarize Survival Data Using Stata Youtube

Factor Variables And Value Labels Stata

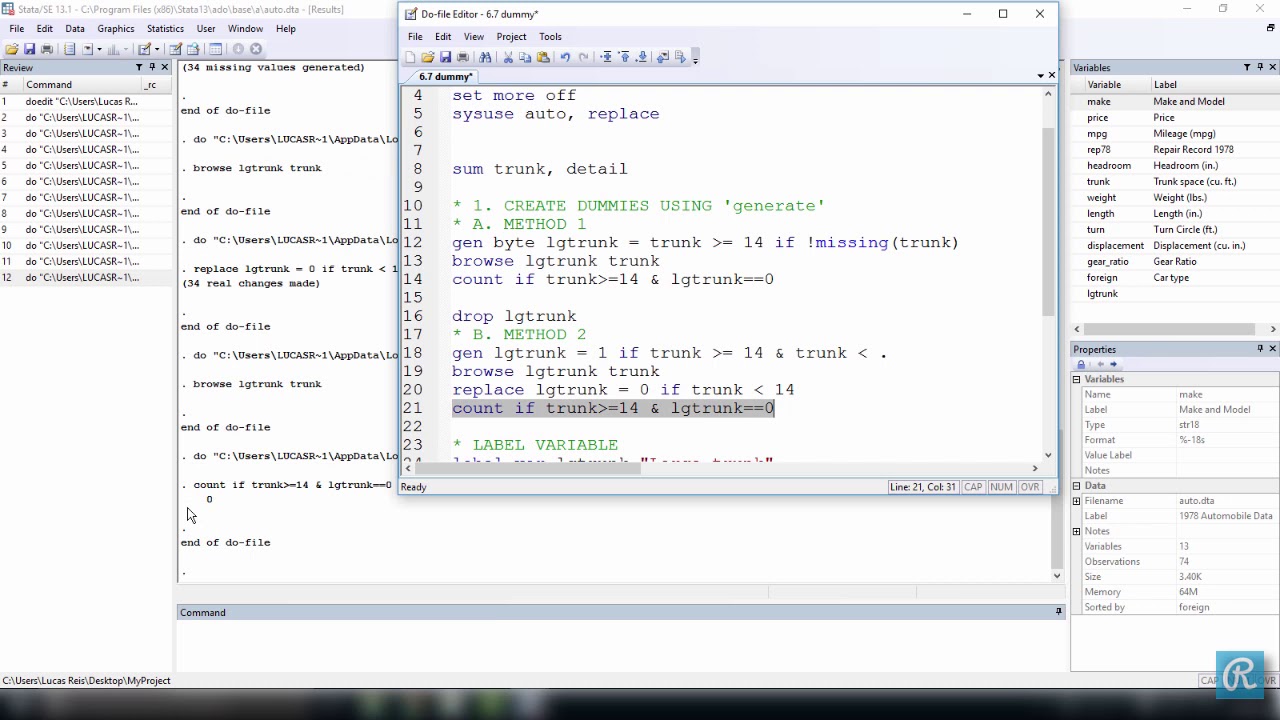

How To Create Dummy Variables In Stata Youtube

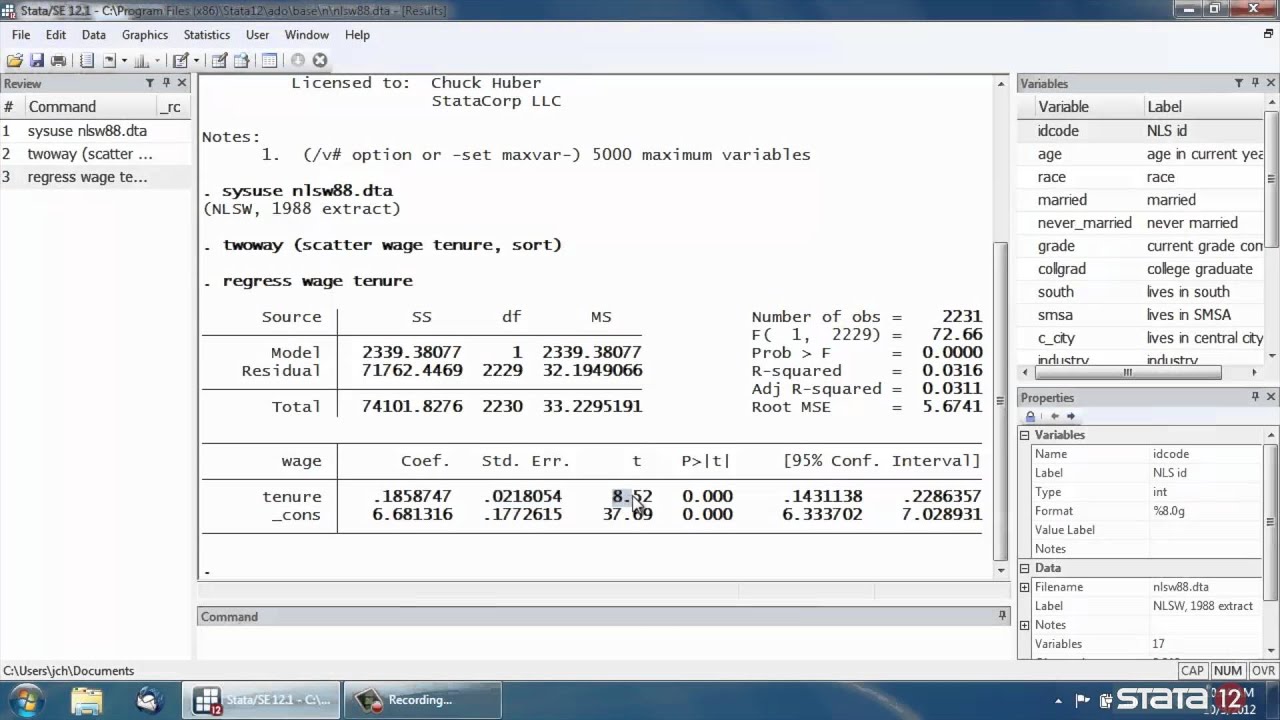

Simple Linear Regression In Stata Youtube

Factor Variables

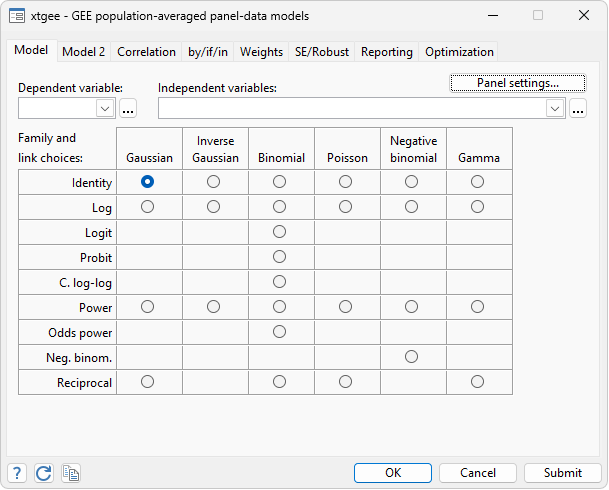

Generalized Estimating Equations Stata

Power Calculation For One Way Analysis Of Variance Using Stata Youtube

Instrumental Variables Regression Using Stata Youtube

Quantile Regression Stata

Power Calculation For Comparing A Sample Mean To A Reference Value Using Stata Youtube

Multiple Imputation

Difference In Differences Estimation In Stata Youtube

Stata Guide Working With Stata

Stata Quick Tip Date Function Youtube

Factor Variables Stata

One Way Anova In Stata Youtube

Endogenous Variables

Endogenous Variables Stata

Komentar

Posting Komentar